Predicting College Student Loan Repayment: The Texas Hinson-Hazlewood College Student Loan Program

by SALVADOR HUMBERTO GÓMEZ, B.S., M.Ed.

APPROVED BY SUPERVISORY COMMITTEE:

DISSERTATION

Presented to the Faculty of the Graduate School of

The University of Texas at Austin

in Partial Fulfillment p

of the Requirements

for the Degree of

DOCTOR OF PHILOSOPHY

THE UNIVERSITY OF TEXAS AT AUSTIN

August 1978

Copyright, 1978, by Salvador Humberto Gómez. All rights reserved.

Acknowledgements

Sincere appreciation is expressed to the many individuals who provided educational, technical, and moral support during the course of my doctoral program of studies. It is impossible to name them all; however, some individuals deserve special mention.

To my supervising professor, Dr. Laurence D. Haskew, is an especially large debt for both his intellectual leadership and his unfailing willingness to expand my meager scholarly potential so that 1% would be reflected in my written endeavors. An equally large debt of gratitude is owed to Dr. Dewey Davis for his knowledgeable critiques, helpful suggestions, and faithful positive reinforcement especially when things were not going just right.

Grateful acknowledgment is extended to Mr. John Romanek, without whose technical computer programming assistance this study would not have been possible. Such grateful acknowledgment is further extended to Commissioner Dr. Kenneth H. Ashworth and to Mr. Mack Adams and his staff from the Coordinating Board, Texas College and University System, for their cooperation in providing this writer with access to necessary data from which to conduct

this study.

Finally, my deepest appreciation is reserved for my wife and our five children who have endured this massive undertaking along with me. Our daughter Rosanna, and our four sons, Salvador, Jaime, Orlando, and Ricardo, have remained firm in their desire to have their Daddy succeed and attain a higher measure of dignity and self-respect. My wife Amelia, whose prayers and ability to withstand hardship and stress during these past four years, proved to be the strongest force behind her sometimes-wavering husband.

To these and to the many Financial Aids Officers, students, and others who because of time and space cannot be mentioned here, I thank you with an equal measure of humility and honesty. The sharing of your perceptions,

opinions, and feelings with a stranger has made this investigation possible.

-S. H. G.

The University of Texas at Austin

July 10, 1978

Chapter I: Rationale, Design, and Operationalization of the Investigation

Introduction

Equalization of educational opportunity has been fulsomely treated in literature of the past decade. (For examples, Coleman and Associates, 1966; Crossland, 1971; Harvard Educational Review, 1969.) It has been common to point to education as a partial solution for poverty although problems of poverty are complex and resistant to cure. One who has summed up the relationship between education and equality of opportunity is John Gardner. "Ultimately," he says, "education serves all of our purposes–liberty, justice and all our other ends–but the one it serves most directly is equality of opportunity. We promise such equality and education is the instrument by which we hope to make good the promise" (4:81). The majority of those who are denied an equal opportunity for higher education, for whatever reason, are condemned to a life of second-rate opportunities, menial employment, and too frequently, unemployment–all adding up to substandard lives for both themselves and their children, it is argued.

Furthermore, the more scientific, automated, and computer-oriented our society becomes, the greater the probability that those deprived of equal opportunity for higher education will suffer (5:1). "Yet," says George H. Hanford, "the most stubborn barrier remains. All our efforts to identify and nurture talent in the minority/poverty communities and all our successes in generating aspirations to higher education will have been naught if there are not the dollars to fulfill those aspirations" (6:vi). If education is to occupy a crucial position in making economic and social parity a reality for the economically disadvantaged, then some means has to be found through which the poor can attain postsecondary education. Financial aid to college students was designed with this end in mind, "to permit college attendance by students who cannot afford to pay the expenses by themselves" (7:5.1).

Boyd, in his report concerning the states' involvement in financial programs, concluded that "state comprehensive assistance programs are in a condition of dynamic change . . . a common thread to all developments is that they provide dollars which permit the financially needy student to attend the college of his choice" (8:28).

One such state is Texas; the passage of the Hinson-Hazlewood Student Loan Act of 1965 created the Texas Opportunity Plan. This was and is a state-supported student loan program designed to "make available to the deserving youth of Texas sufficient financial resources to finance the college students' share of the cost of their college education" (9).

The origin and development of governmental programs for loans to postsecondary students are traced inconsiderable detail within Chapter II of the present report. As pointed out there, loan programs are only one variety of governmental programs designed to provide financial aids to penurious would-be students in colleges and universities, in an effort to pursue a social goal of equalizing access to opportunity for education.

Origin of This Investigation

As elaborated upon in Chapter II, public policy to furnish loan programs was predicated on, among other things, an assumption that loans and interest thereon would be repaid by the borrowers. Presumably, this meant taxpayers per se would not be called upon for heavy financial support. As time elapsed however, the repayment patterns of borrowers did not match this assumption. Volumes and incidence of non repayment mounted steadily above those pre estimated. In 1973-1976, the default rates were being highly publicized across the United States. Federal and state government policymakers–as well as institutional loan administrators–were beginning to wonder aloud if the public policy decision had been a mistake. These officials concerned most with the preservation of this policy–legislators, ministerial executive agencies, and institutional loan program administrators–began to search for ways and means to reduce the incidence of non-repayment behavior to levels tolerable for the political system.

The investigator was, and is, one of these concerned, as the Financial Aids Officer for one university in The University of Texas System. He participated in meetings and task force appraisals aimed at reducing the problem of borrower delinquency. As a result, he became (a) rather fully aware of the dimensions of the delinquency problem and suggested means for minimizing it, and (b) much interested in contributing toward the preservation of government student loan programs by investigation of possible "causes" for borrower delinquency.

The Investigation Contemplated

The first task, of course, was to identify a college student loan program to serve as proxy for all governmental loan programs to serve as proxy for all governmental loan programs and the patrons thereof. Naturally, the investigator leaned toward the most convenient one, the Texas Hinson-Hazlewood College Student Loan Program (the successor to the original Texas Opportunity Plan). Comparative examination revealed that its core characteristics were similar to those of other state programs participating in the United States Department of Health, Education, and Welfare’s Guaranteed Student Loan Program. Officials at the coordinating Board, Texas College and University System (the ministerial executive agency for the Texas Hinson-Hazlewood College Student Loan Program [ HHCSLP] were warmly supportive and encouraging toward the utilization of stored data and retrieval facilities. The investigator’s supervising professor also thought the HHCSLP would be a valid proxy, and the first design task was completed by choosing HHCSLP as the referent loan program. A thumbnail sketch of features of HHCSLP follows.

The Texas HHCSLP

The Texas Opportunity Plan, later named the Hinson-Hazlewood College

Student Loan Program (HHCSLP),provides long-term educational loans to Texas residents. To be eligible for a loan, the applicant must be enrolled in or accepted for enrollment in an approved Texas public or private institution of higher education.

The Coordinating Board, Texas College and University System, a state agency, administers the program through a set of Rules and Regulations adopted for this purpose. Each participating college or university is required to appoint an on-campus official who serves as the HHCSLP Officer. This officer, typically the Director of Student Financial Aid, is responsible for the administration of the HHCSLP on campus. Applicants, therefore, secure loans at the Offices of Student Financial Aid in the participating institutions.

To be eligible for an HHCSLP loan, individuals must meet the following requirements:

- Be a legal resident of Texas.

- Be enrolled or accepted for enrollment for at least one-half of a normal academic course load in the participating college or university. If enrolled, the student must be meeting the minimum academic requirements of the institution.

- Establish that he or she does not have sufficient resources to finance a college education.

- Be recommended by two reputable persons in his home community.

- Be recommended by the Texas Opportunity Plan Fund Officer at the participating college or university where the loan application is made. (10)

The amount of a student's loan cannot exceed the difference between the financial resources available to the borrower and the amount necessary to meet reasonable educational expenses as a student. The financial resources considered available to the student include all forms of financial assistance which may be received from any source. A student may borrow a maximum of $1,500 per 9-month school year. Loans of up to $500 are available for students to attend summer school. The total outstanding loan principal due to the State of Texas may not exceed $7,500 at any time.

The 1975 interest rate on loans was 7 percent per annum. Loans are insured by the federal government; if borrowers qualify for the interest subsidy, the government will pay the interest until the student is placed in repayment status. Students are placed in repayment status nine months after they either graduate or leave the institution. Students who do not qualify for the interest—subsidy must pay interest periodically while enrolled and until they are placed in repayment status; at this time it becomes a part of their monthly repayments. To be eligible for the interest subsidy, the student's adjusted family income, as reported on the federal loan application form, may not exceed $15,000 per year. Payments of interest charges for students who qualify for the ¡interest subsidy are made by the federal government directly to the HHCSLP. For an insurance premium, the HHCSLP pays 0.25 percent of the principal for each loan to the federal government agency.

Regardless of the date of loan award, repayment must begin no later than nine (9) months after the borrower is no longer enrolled in an institution of higher education. Payments are made direct to the Coordinating Board in amounts of not less than $30.00 per month. The loan repayment period cannot exceed ten (10) years from the date a borrower last enrolled in a participating institution. All principal is due and payable 15 years from the date of the first note unless special permission is given by the Commissioner of Higher Education to extend the term beyond the 15-year term. Such special permission may be granted for continuing education, military service or financial circumstances. Medical, dental, or other professional candidates seeking an advanced professional degree may secure such special permission, provided proof of acceptance and enrollment in such a degree program is provided to the Commissioner.

To be eligible, an applicant must present letters from two "reputable persons" recommending the applicant for a loan. Information-procuring forms and declarations prepared by the Coordinating Board must be executed; institutional officers may require additional relevant information. These materials attempt to assure that borrowers know they are executing contract(s) for repayment of a loan, and are not receiving a grant. Also, the forms attempt to make clear that the loan is made by the State of Texas, not by the institution. When the applicant is officially accepted for enrollment or enrolled, the Texas Opportunity Plan Officer completes the institution's part of the application forms and submits them to the Coordinating Board for final approval. Upon approval a payment check is sent to the institution, but disbursed to the student only after the student's enrollment status is again verified. When a borrower is eventually placed on payout status, the Coordinating Board prepares the payment cards, mails them to the borrower along with a repayment schedule explaining to him or her how and when to make payments. If a student defaults, the Board is empowered to resort to legal action in order to collect.

The volume and seriousness of borrower default in repayments to HHCSLP are documented by the fact that as of February 1, 1975, Coordinating Board officials had requested the Attorney General of Texas to file legal actions against 7,650 borrowers in repayment status, entailing 9.48 percent of the principal and interest value of all loans extended since inception of the Texas Opportunity Plan and $10,035,793 in money due to the HHCSLP (11). The Texas 9.48 percent of default compares unfavorably with other state student loan programs whose average default rate was 5 to 7 percent in 1973, but more favorably with the national average default rate of 14 percent for the federal government's Guaranteed Student Loan Program reported on January 13, 1973 (11, 13).

The lending capital for the HHCSLP is provided by the sale of General Obligation Bonds of the State of Texas, the authorization of which must be by an amendment to the Constitution of the State of Texas presented by the State Legislature and ratified by a vote of the people. Details of this and other developmental features of the HHCSLP are provided by Chapter II of this report.

The Contextual Framework

The second pre design task was for the investigator to set a context, that is, "a reason why" he was investigating. A few other doctoral dissertation investigations in the student loan default area had been studied. Their context seemed to be that of searching for correlations between descriptors of borrowers and defaults by borrowers. The reports terminated by reporting statistical correlations, or relationships, and somewhat frustrated this investigator by raising, "so what" skepticisms in his mind. He wanted to achieve more than that. He wanted to offer something that might affect public policy, policies of ministerial agencies, and/or institutional administration of student loan programs. All he would have to offer, however, was information and derivations therefrom.

A11 three targets for his desire–public policy, policies of ministerial agencies, and policies/practices, of institutional administration–lay within political systems. In fact, each was a focal processor of input whose output was authoritative governance. "Inputs" gave the clue. One input common to these decision makers was information. If information was deliberately beamed toward solving a problem–such as that of reducing loan default rates–perhaps it could be influential toward outputs, the investigator reasoned. After conferring with members of his supervising committee, he saw that the distinction between his style of study and that referred to above would have to be that of (a) constantly asking, "of what utility (in the practical sense) is the information to decision makers?" and (b) digging much deeper than others have done below the surface of statistical data, using common sense. Those perceptions furnished the essential context descriptor–"findings which are utilitarian for political system decision rendering."

He then went to standard literature on political system decision making and located the Easton Model which, better than those focused upon interperson and intergroup dynamics, seemed to be adequately explanatory of what the investigation would be about. In his Framework for Political Analysis, David Easton offers and explains a “Model for Political Analysis'' (14:7ff). A paradigm representation of this model appears in the following page of this report.

It indicates that the systems within the total environment produce inputs to the political system. Federal, state and/or local governing bodies could be considered the Authorities. An equal educational opportunity could be one of these demands (Inputs), and financial aid could be an Output that is designed to satisfy the environment in response to the demand. Outputs are intended to modify environmental conditions so that the

original circumstances that gave rise to the demands no longer exist, or they may . . . create this impression in the minds of the members, even though in fact nothing other than the image has been changed. (14:127)

The goals of the Authorities are of course to satisfy the environment's demands with positive outputs that will be rewarding to them, i.e., in future elections, and satisfying and beneficial to the environment. The Authorities learn about the consequences of their outputs from information that returns from the environment and eventually flows to them.

. . . there must be a continuous flow of information back to them so that whatever their goals may be with respect to support or the fulfillment of demands, they are aware of the extent to which their prior or current outputs have succeeded in achieving these goals. (14:129)

Easton goes on to say:

With respect to the input of support, we cannot take the goals of the authorities for granted. The authorities need not always be eager to encourage support for a system. . . . However, in some instances the authorities may well be interested in modifying the system radically, or destroying it entirely. (14:129)

Negative feedback, as spawned in the case of excessive interest rates, the declaration of bankruptcy by student borrowers coupled with the existing demands from the environment to place more controls on student loans could conceivably have the "authorities" curtail, modify or repeal student loan legislation.

Thus, the pervading contextual purpose of the present investigation is to introduce information which is useful to Authorities into the Feedback Loop of the model. At present, a previous policy decision (an output) to provide loans to students is arousing consequences which, when information on them is transmitted by the Feedback Loop as inputs, is placing a demand for corrective action upon the Authorities. But information indicating what, if anything, needs correcting is scanty. The investigation contemplated would seek to overcome some of that deficit.

The Investigative Problem

The initial problem stated for the investigation was quite simplistic: "What causes borrower defaults?" This question assumes there are "things" which impact borrowers who default and do not impact so strongly borrowers who repay. However, it was seen, only some "things" may be correctable. In response to the contextual purpose, the question was revised: "What correctable 'things' cause borrowers to default?" Still further difficulty arose. "Things" might be correctable, but the means available to correct them might do more harm than good. For example, a regulation which removes a cadre of borrowers from eligibility might cancel out large numbers of deserving borrowers who will repay. Hence, "constructively" was placed in front of "correctable."

The greatest difficulty with the original statement, however, was the word "causes." Its use would propel the investigator into a never-never land; cause-effect is almost impossible to trace in accounting for human behavior. About the best that can be done is to show cooccurrence between one "thing" and another "thing." For example, taking out a large loan is associated, at greater than random levels, with subsequent default. Obviously, taking out a large loan may be only a symptom of a personhood syndrome or of a set of pressing real-life circumstances which constitute the "cause" of default (if there is actually anything which is the cause of default, which is doubtful). This led to the final operational statement of the investigative problem:

What "things" are significantly associated by co-occurrence with borrower defaults, and which of these are constructively correctable by the authorities?

Analysis of the Problem

Already given was the fact that the HHCSLP and its borrowers would furnish the proxy data to be used by the investigator to test defaulters against "things" for significant cooccurrences.

“Cooccurrences" could not be established as significant without the presence of a population of nondelinquents to compare with a population of delinquents. That necessitated an operational definition of HHCSLP non-delinquents and delinquents in the investigative design. The respective subpopulations would be those borrowers shown as delinquent and nondelinquent on the August 3l, 1976, loan roster.

"Things" to be tested for co-occurrence with being delinquent also had to be operationalized, i.e., defined and selected for the investigative design. This definition is set forth in the next section of this chapter.

"Correctable" had to be interpreted. Determination that a given "thing" can be eliminated or reduced by means available to the Authorities could not be reached empirically, it was assumed. The determination would be by subjective acts-of-mind on the part of the investigator supported by knowledge of real life and deductive logic."Constructively" would likewise be a subjective argument, resting upon empirical evidence gathered by implementation of the investigative design.

"Authorities" also had to be defined operationally. They would be (a) the Texas Legislature, (b) the staff plus Board of the Coordinating Board, and (c) institutional loan administration.

Operationalized Purposes of the Investigator

Obviously, the broad purpose of the investigator was to produce some answers to the problem-question appearing in The Investigative Problem (above).

Analysis of that problem and the contextual framework produced the following operationalized purposes as marching orders for (a) the investigative design, and(b) the dissertation report. These are stated in product format:

- A synthesized portrayal of the origins and nature of the governmental student Loan movement and its resultants in public policy, ministerial policies and consequences, including delinquency in repayments of borrowers.

- Identification of a set of "things" potentially entering into borrower decisions to become delinquent, limited to "things" whose existence can be measured by data procurable from HHCSLP sources.

- Testing the degrees of cooccurrences between these "things," on the one hand, and the prevalence of these things in nondelinquent and delinquent borrowers from HHCSLP, on the other hand.

- A report upon the significance/nonsignificance of cooccurrences with respect to (a) being predictive of non delinquency or delinquency, (b) the extent to which cooccurrences are utilitarian for political system decisioning, and (c) the utilitarian implications of the total array of findings.

- Derivations from the evidence gathered and the experience of the investigator which seem to have consequence for future efforts to reduce repayment delinquency.

The Investigative Design

Sources for Evidence

Three sources were selected to provide some cross-checks upon cooccurrence yields, as well as to produce data more comprehensive with respect to "things" than could be procured from any single source.

Financial Aid Officers in HHCSLP-approved institutions comprised one source. Utilizing a simulation instrument, they forecast the prevalence of 26 "things" in a simulated population of delinquency borrowers compared to an equal-size population of non delinquent borrowers. They were asked to use such hard facts as they had, supplemented by derivations from their observation of borrowers over time.

Borrowers who were, as of August 31, 1976, in repayment status for an HHCSLP loan comprised the second source. A delinquent and a nondelinquent subpopulation established the presence/absence of named "things" as characterizing their in-college and post college experience. Details of the compositioning of the two subpopulations appear in Chapter III of the present report.

The third source was recorded information on borrowers possessed by lending institutions and/or the Coordinating Board. The information was procured for sub-populations of non delinquent and delinquent borrowers.

Details respecting the sampling controls appear in Chapter III.

The "Things" Population

Obviously, it was necessary to have a predetermined set of variables in order to procure comparable data. "Things" was therefore operationally defined as "variant factors, conditions, and/or experiences' ' attached to being a college student and an HHCSLP borrower. It is difficult to draw a firm boundary between these three categories. In the investigator's mind as he searched for putative influences, factors pointed toward semi demographic accompaniments (e.g., family in lowest socioeconomic status; age at date of first loan; borrowed while in a large college). Conditions pointed to circumstantial accompaniments (e.g., number of dependents increased; parents divorced after loan). Experiences pointed to personal encounters, behaviors or conclusions (e.g., assumed loan really would not have to be repaid; disappointed in securing adequate employment). In the texts of Chapters II and IV, the words "factors" or "variables" are used often, in the interest of brevity, to refer to the "things" used as procurers of data.

The task of compiling the list was of major size in the investigative design. As previously noted, the investigator had participated extensively in discussions of the problem of repayment delinquency. He was able to produce a large number of suspect variables which had been pointed to in those discussions. He asked several colleagues, as well as knowledgeable officers in state and national government, to nominate suspects. He consulted every published account of research on the subject he could find (see Chapter II). And he and his supervising professor brainstormed considerably. One of the troubles was that almost every item nominated overlapped other items. The long list of suspects was reduced by combining items, and still further reduced drastically by asking, “Can data establishing the existence of this item be procured within the limits of available time and funds?"

Parenthetically, this latter experience may be as important (though not documented) as any other finding made from the investigation. A very high proportion of a11 suspect variants is non-utilitarian toward strategic or tactical decisions, because data with which to measure their presence/absence cannot be procured within real-life practicalities.

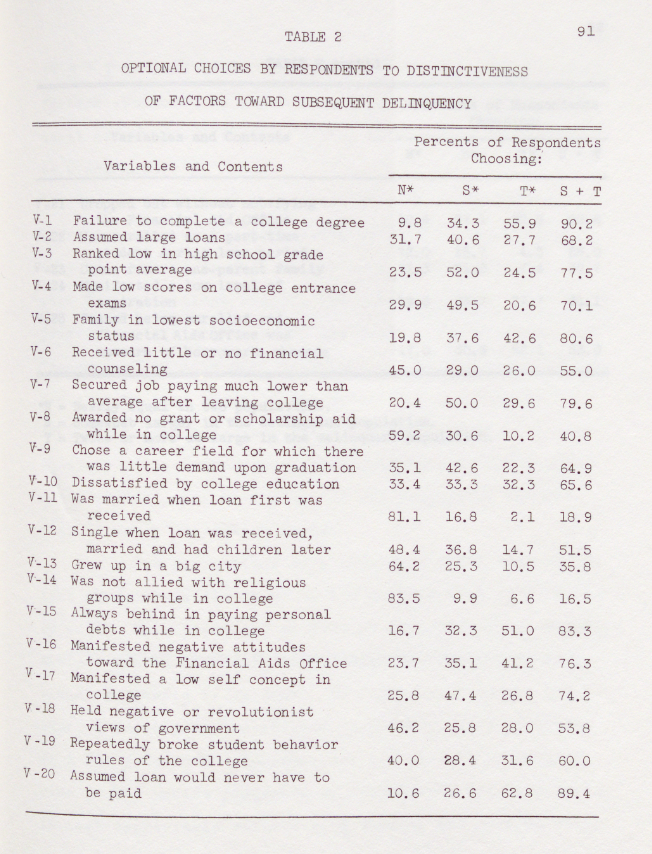

Eventually a final list was arrived at. Its contents may give overemphasis, numerically, to "things" reflecting lack of diligence on the parts of institutional lenders. At the time, lack of loan-officer diligence was a favorite whipping boy. Otherwise, the variables in total were reasonably balanced between the types of "causes" alleged. To conserve space, the list is not presented here. In totality, it appears in the Questionnaires appearing in the Appendix. For the purposes of comparing data-source reports, the total list was telescoped down to 33 variables. These are displayed by Table 11 in Chapter III.

Instrumentation for Data Procurement

For the Financial Aid Officers' source, a novel simulation-based opinionnaire was developed, and it appears in the first pages of the Appendix. Its schematic was to write out an occasion for predicting the proportionate presence of each of a set of suspect variants in a population of delinquent borrowers compared to a population of nondelinquent borrowers. The variables were carefully phrased to communicate to the prospective respondents. The directions to respondents called for coded responses which were quantifiable along a continuum from “decidedly more" (delinquents would show this than would nondelinquents) to "decidedly less." The wording was constantly checked with willing colleagues and the supervising professor for clarity and communicative effectiveness. These checks occasioned successive revisions until a high mark from jury members was received. The instrument, along with a cover letter of request, was mailed to 136 Financial Aids Officers. Information comparing respondents with the recipient population appears in Chapter III.

For the Borrower source, a mail-out questionnaire was also used. The final instrument appears as Questionnaire II in the Appendix. It is much simpler than the Financial Aid Officers' instrument, appearing essentially as a list of experiences for respondents to code as matching or not matching their own experiences. In selecting the items, the investigator was very careful not to include any which would possibly ire delinquent borrowers and thus reduce or bias responses. The instrument itself went through the same revision process described in the preceding paragraph, with some students joining the "¿jury." When finalized, it had such appeal and promise to staff of the Coordinating Board that it was transmitted as a request from that agency for "helpful information." Information on the mailee and the responding populations is given in Chapter III.

The Institutional Records source was tapped by a "Request for Data" form transmitted to each HHCSLP lending institution. A Borrower Population sampling delinquent and nondelinquent subpopulations was drawn by the investigator (details in Chapter III). These names were allocated to the institution of first loan, being entered in random order on the respective request-for-data form. The form provided columns for entering requested data after each student name. Definitions for data requested accompanied the form. The instrument appears just after the Questionnaire III in the Appendix. Information on the solicitee and responding population is provided in Chapter III.

Treatments of Data

Throughout, the treatment of data was constrained by the necessity to compare the incidence and relative prevalence of factors, conditions, and experiences in two subpopulations–non delinquent and delinquent–of borrowers. It was expected that regardless of the source of data, some members of the delinquent subpopulation and the nondelinquent population would be in every distribution cell. The investigator, in treating and in interpreting the data, had to keep forever before him the fact that he was not comparing individuals but whole populations.

The raw data from each individual respondent were to be transferred to a computer input card and thence to tape storage. Computer programs would produce respective subpopulation and "all borrowers" numerical frequency distributions, by code, for each variable; calculate proportionate (percent) distributions of two types: (a) subpopulation members accounting for each of the code frequencies, (b) each subpopulation distribution between code options. This information would be stored and drawn upon by computer programs in calculating degrees of differences between subpopulations in the way their members were arrayed with respect to each variable. Chi-square methodology was to be used to ascertain the statistical degree of difference and to produce the index of difference was not likely to be a function of chance. Thus, it would be discovered which variables, if any, gave statistically significant differences in readouts from the two subpopulations–supporting conclusions that a given variable was or was not predictive with respect to borrower status.

However, the investigator would not forget his utilitarian framework. He would use percent distributions and member-frequencies to further analyze the data which produced "significant" differences of various degree and thus test the utilitarian value of the "predictiveness by cooccurrence" apparently existing. This, in turn, would assist in discovering hunches which might be translated, by logic, into derivations beyond the evidence actually secured.

For final summative purposes, the investigator would employ a four-cell classification for the predictive potency of variables: Not Predictive; Mildly Predictive; Considerably Predictive; Strongly Predictive. This device, with its definitions and applications, is described more fully in Chapter IV.

The investigative design described was implemented. This dissertation report includes the results produced from the design.

Arrangement of the Report

Chapter II is a documentation for the background from which this investigation emerged. As indicated, it portrays the genesis and development of the student loan movement and the public policies it spawned.

Chapter III is the traditional "research" chapter. It treats separately each of the three sets of data obtained, respectively, from Financial Aid Officers, Borrowers, and Records. The findings from each are presented and interpreted. Summation of the three sets of findings,however, is pushed forward to Chapter IV.

Chapter IV may be described as the investigator's chapter, in which he puts himself into the findings and tries to extract significance and derivations of considerable import.

References

- Coleman, James S., et al. Equality of Educational Opportunity. Washington, D.C.: U.S. Office of Education, 1966.

- Crossland, Fred E. Minority Access to College: A Ford Foundation Report. New York: Schacken Books, 1971.

- "Equal Educational Opportunity," Harvard Educational Review 39, no. 2 (1969).

- Goals for Americans: The Report of the President's Commission on National Goals. Englewood Cliffs, N.J.: Prentice-Hall, Inc., 1967.

- Wright, Stephen J. The Financing of Equal Opportunity in Higher Education: The Problems and the Urgency in Financing Equal Opportunity in Higher Education. New York: College Entrance Examination Board, 1970.

- Hanford, George H. Financing Equal Opportunity in Higher Education. New York: College Entrance Examination Board, 1970.

- Manual for Financial Aid Officers, Part Five: "Need Analysis.'" New York: College Entrance Examination Board, 1971.

- Boyd, Joseph D. "20 States Aid Students,” College Management 5, no. 3 (1970): 21-30.

- Section 506, Article III of the State Constitution and Chapter 101, Acts of the 59th Legislature, 19659 (compiled as Article 26549, Vernon's Annotated Texas Statutes). Austin: The State of Texas, 1975.

- Coordinating Board, Texas College and University System. Rules and Regulations of the Hinson-Hazlewood College Student Loan Act. Article III, Section 1, Austin, Texas, 1971.

- Adams, Mack. Head, Student Services Division, Coordinating Board, Texas College and University System. Interview, February 27, 1975.

- Winkler, Karen J. "Defaults Up," The Chronicle of Higher Education, September 30, 1974, p. 7.

- Bell, Dr. Terrell. U.S. Commissioner of Education, as quoted in "Student Loan Millions Asked," The San Antonio Express, February 24, 1975, p. 2A.

- Easton, David. A Framework for Political Analysis. Englewood Cliffs, N.J.: Prentice-Hall, Inc., 1965, p. 110.

Chapter II: Background of the Investigation

Section One: Evolution of Financial Aid to College Students

Financial aid to students has a history almost as old as that of higher education in America. Early programs of student aid in American colleges were started with money provided specifically by private individuals and groups to aid needy and worthy students. The original purpose of student aid was to make a college education available to any otherwise qualified individual who could not himself pay for the cost of attending college. Rudolph comments that

the college was not to be an institution of narrow privilege. Society required the use of all its best talents, and while it would, of course, always be easier for a rich boy than a poor boy to goto college, persistence and ambition and talent were not to be denied. The American college, therefore, was an expression of Christian charity, both in the assistance it gave to needy young men and in the assistance it received from affluent old men. (1)

Programs of financial assistance for students in America can be said to have begun in 1643 when Lady Anne Mowlson gave one hundred pounds to Harvard during its early days and set up the first student assistance endowment fund in an American college. "With this somewhat unfortunate and illfated beginning, American colleges began the practice of financing students" (2).

Between 1643 and until about the time of the Civil War, student financial aid underwent its first era of trying to identify itself in the social setting. American colleges had inherited many of the aristocratic goals, purposes, and customs of the English residential colleges. That, it was soon discovered, did not fit into the developing democratic society of the America of that day. As the American college slowly evolved into a democratically oriented institution, it began to receive increased amounts of both private and governmental support, with some of the support taking the form of recognizable, overt student aid (2:2).

Democratic idealism gave colleges and universities a much broader social purpose than institutions of higher education had previously known. With time, this social purpose developed into a national purpose. More

and more poor young people began attending college in quest of an education as a means of changing their economic conditions. This trend alarmed some of the more "aristocratic” citizens. A South Carolina editorialist stated, "if the state sets up a college, learning would become cheap and too common, and every man would be for giving his son an education” (1:20).

However, as early as the latter part of the eighteenth century, the Harvard College chapter of Phi Betta Kappa established a fund for the aid of indigent members (2:5). Later at Brown University, a society was organized for the purpose of lending textbooks to poor students. In some colleges, special dining halls were set up to help needy students.

Another form of student financial aid to emerge during the early days was that of manual labor. "The notion that young men could earn enough money to pay their way through college gained rapid support" (2:3). This notion appears to be the foundation of what much later became cooperative education and college-work-study programs.

Immediately following the Civil War, the "popular" colleges emerged. They were established for the purpose of meeting the expanding need for technical and scientific education which had been produced by the Civil War. One of these was the Massachusetts Institute of Technology (2:6). The Morrill Act of 1862 put federal largess at the disposal of every state government. Funds derived from this legislation were designed to develop in the land-grant colleges after the Civil War a "new network of institutions” with a popular or practical orientation (2:7). And, by making the colleges popular and more desirable, it placed a new burden on the tradition of student aid and argued forcefully for the maintenance of equality of access to higher education.

The first significant example of state-funded student financial aid after the Civil War came with the state legislatures providing free tuition to Civil War veterans at state colleges and universities (2:7). AT about this same time, private institutions began to receive their first endowments for purposes of student financial aid from America's first "corp of millionaires" (2:7). Harvard President Charles W. Eliot, in his inaugural address at Harvard in 1869, remarked that "no good student need ever to stay away from Cambridge or leave college simply because he is poor . . . the recipient must be of promising ability and the best character . . . the community does not owe superior education to all children, but only to the elite . . . to those who, having the capacity, prove by hard work that they have also the perseverance and endurance" (3).

Later, the category of loan funds was added. This became a particularly attractive form of student aid to a generation that was '"wedded not only to the myth of the self-made man but to some equally pervasive myth that came under the label of social Darwinism" (2:8). The belief of that day was that loans did not damage individual character as much as did scholarships and other direct forms of student aid. Governor Lucius Robinson of New York remarked in 1877 that, "loans taught obligation, while scholarships and other forms of free higher education might fill the masses with discontent, unsettle their purposes, and destroy their initiative" (4).

In the twentieth century, the American tradition of student aid for higher education climaxed with an ever increasing effort to make higher education available to all who would seek it. Rudolph explains it this way:

The federal government in this century has used student aid to fight a depression, to thank the veterans of two wars, and to shore up the national defense. Some state governments are transplanting student aid into networks of colleges; municipal institutions dispense with tuition charges; local committees, high schools, and service clubs distribute aid funds of their own. Alumni groups, foundations, and business concerns multiply their exertions in behalf of the American college student. (2:1)

Federal Government Activities

The idea of the federal government's providing direct financial aid to students is relatively new. During the days of the Great Depression of the 1930s numbers of students were aided through such agencies as the National Youth Administration, but programs of this nature were short lived.

During World War II, the federal government made some eleven thousand loans to students in selected fields of study in an attempt to maintain interest and enrollment in curricula of vital need to the national security (5).

In the closing months of World War II, the Servicemen's Readjustment Act of 1944, better known as the G. I. Bill, was passed. This action, taken by a grateful citizenry, allowed a large number of students to attend college with a very substantial direct support from the federal government granted without regard to financial need (6). Since the passage of the first G. I. Bill,

Similar legislation has been enacted for veterans of the Korean conflict as well as the Vietnam War.

Other federal legislation in 1958, as an outgrowth of Sputnik, and in 1965, as an outgrowth of the Civil Rights movement, involved the federal government still more in the role of providing financial aid to students (7).

A series of federal enactments designed to aid needy students in higher education began with the National Defense Education Act of 1958. Title II of this act created the National Defense Student Loan Program. The initiation of this program marked the beginning of a new era in massive federal aid to students in institutions of higher education, and indirectly to higher education itself.

Funds from this program were intended to aid students seeking baccalaureate degrees in engineering, mathematics, modern foreign languages and education. The pattern of selecting loan recipients was similar to that for scholarships. However, as time passed, affording preferential treatment to academically superior applicants was no longer mandated by the Act. This represented an important shift in the rationale behind most college financial aid programs, and particularly those programs funded in part by the federal government. Financial need became the primary criterion for eligibility.

Since its enactment, the National Defense Education Loan Program has been the backbone of all federal government programs for student aid. It has grown from an initial $6,000,000 appropriation in 1959, to a $293 million appropriation for the 1974 fiscal year (8) (9).

The passage by Congress of the Higher Education Act of 1965 added some new dimensions to the trends in student aid programs in higher education. It created a program of grants for undergraduates, and a student employment program. In addition to continuing the National Defense Student Loan program, it created also a federal government program to guarantee the repayment of loans by students as well as to pay interest subsidies to lenders on loans made by private or public agencies. This became the Guaranteed Student Loan Program, and was also the earliest legislation that "accepted as a national purpose the opening of opportunity for postsecondary education to all qualified students" (7).

This legislation prompted many private lenders to involve themselves in the business of providing financial aid to students. Some saw it as a long-term investment in future business, others did it as a means of supporting sons or daughters of "long-time"” customers.

States also began creating their own student loan programs in the middle and late 1960s. These state loan programs multiplied and by 1974 there were 24 state supported loan programs in existence (10). Some of these programs were insured by the federal government's GSLP, some were not.

The State of Texas created its student loan program, the Texas Opportunity Plan (later named the Hinson Hazlewood College Student Loan Program), in 1965 (12).

Section Two: History of the Hinson-Hazlewood College Student Loan Program

The Texas Hinson-Hazlewood College Student Loan Program was fashioned after the Opportunity Plan, Incorporated (OPI), originally initiated at West Texas State University at Canyon, Texas. The OPI was designed, organized and eventually implemented from 1961 to 1970 by Milton Morris, the Director of Student Assistance at West Texas State University. The OPI was created from private contributions. It was designed to provide loans to students attending that university (11).

Mr. Morris stated that he, like Governor Lucius Robinson, believed that loans were better than grants as a means of molding character through responsibility whenever possible. While he wanted to provide students with financial assistance, he also wanted to teach the students to manage their personal finances as they received their education.

Students receiving loans under the West Texas State University OPI were required to submit a budget estimating their expenses prior to the beginning of every semester. Once the budget was approved, the loan was set aside for the borrower in the amount necessary to cover the expected expenses. The student would accept the check for the loan, and then deposit the money, in his name, at the OPI Program Office. The student was asked to keep a record of his expenses; these records were checked three times during the semester. As student borrowers and/or depositors needed money for the expenses outlined in their budgets, they would draw against their OPI accounts. The purpose of turning the money over to OPI was to keep the students from spending their money on items other than budgeted ones, or from exhausting their resources before the end of the semester (11).

Upon graduation or leaving the institution, students executed a promissory note and agreed to a monthly installment repayment schedule. The money borrowed carried no interest and students were given a grace period of several weeks after leaving college before their first payment became due. This allowed students time to secure a job and get somewhat settled before their monthly installments began.

Mr. Morris conceived an idea of creating a statewide student loan program, and discussed it with the state senator from his district, Senator Grady Hazlewood. Senator Hazlewood arranged for Mr. Morris to meet with Governor John Connally at Austin. Mr. Morris suggested to the Governor the necessity for such a state loan program. Governor John Connally, in his opening message to the 59th Legislature, proposed establishment of a statewide college student loan program (12). Representative George Hinson of Mineola authored and sponsored the necessary legislation in the House of Representatives. Senator Grady Hazlewood of Amarillo authored and sponsored corresponding legislation in the Senate (12).

The joint resolution sponsored by Representative Hinson and Senator Hazlewood proposed an amendment to Article III of the Constitution of the State of Texas creating the Texas Opportunity Plan Fund. This was passed by the Legislature and the proposed Constitutional Amendment was submitted to the voters of Texas on November 2, 1965. It provided for the sale of general obligation bonds of the State of Texas not to exceed $85,000,000 (12). The amendment was publicly endorsed by the Coordinating Board, Texas College and University System. It was passed by the voters. The Coordinating Board was charged with full administrative responsibility for the Texas Opportunity Plan, and work was begun immediately to implement this new responsibility (12).

An Advisory Committee on Student Loan Procedure was appointed by the Coordinating Board on November 15, 1965; the Coordinating Board also set September, 1966, as the date on which the first loan was to be made. The First Southwest Company of Dallas was selected to serve as financial advisor in February, 1966. The law firm of McCall, Parkhurst and Horton was selected to serve as the state's legal counsel in regard to insurance and sale of

the bonds (12:8).

On July 18, 1966, $10,000,000 in bonds were sold at an interest rate of 3.77392 percent to Harris Trust and Savings Bank of Chicago (12:8). The Texas Opportunity Plan (later renamed the Hinson-Hazlewood College Student

Loan Program) was therefore established and funded. Having worked out financial details, the Coordinating Board instructed its staff to design a set of lending and collecting procedures, and the necessary forms to be used in administering the program. Subsequently, workshops were conducted throughout the state to explain the loan program to Financial Aids Officers at the institutions of higher education which had requested participation in the program (12:8).

The original rules and regulations for the program required that an applicant:

- be a resident of Texas.

- complete an application for a loan on the forms provided by the Commissioner.

- be enrolled in a college for at least half time.

- establish that he or she had insufficient resources to finance his/her college education.

- be recommended for a loan by the financial aid officer at the institution where the student is enrolled or accepted for enrollment. (13:10)

In addition to the above, the rules set a loan ceiling of $5,000 for undergraduate students and an additional $2,500 for graduate students. The total loan to any individual student in any academic year was not to exceed $1,500 to a graduate or professional student or $1,000 to an undergraduate student (13:12).

Five years was set as the maximum length of time a borrower was to be allowed to retire the loan (13:14). Borrowers were to be placed in repayment status four months after they either left the institution or ceased to be enrolled on at least a half-time status (13:15).Fifteen dollars per month was set as the minimum monthly payment, with payments varying in direct proportion to the size of the loan and the five-year repayment period (13:15). For each $1,000 borrowed, $1.44 per year was to be charged for life insurance that would guarantee the repayment of the loan in case of the borrower's death or permanent disability (13:19).

In September, 1966, the Coordinating Board was approved by the U.S. Office of Education as a lender under Title VI-B of the Higher Education Act of 1965. With this approval, Texas Opportunity Plan loans became subject to federal government interest subsidy. The federal government agreed to pay the full 6 percent interest (as set by the Coordinating Board) charged on loans to a qualified student so long as the student continued to be enrolled on at least a half-time basis. Once the student entered into repayment status, the federal government was to pay one-half the interest charges (12:10). Interim notes were to be executed by the borrower upon receipt of each loan. The originals of these interim notes were to be kept at the institution with copies going to the Coordinating Board. Pay-Out Notes were to be completed at the time a student no longer intended to borrow from the program.These Pay-Out Notes covered the total of all loans, interest, and insurance cost. The original copy of the Payout Note, along with all original copies of Interim notes, were then to be sent to the Coordinating Board. Before preparing a Pay-Out Note, the institution would request from the Coordinating Board a summation of all loans entered into by the student. The Coordinating Board would then provide the institution with the total amount that was to be used on the Pay-Out Note (13:14).

An Exit Interview Form, containing the student's name and address, the names and addresses of his parents and two close relatives, employer name and address, and plans for the next two years was to be completed by the student upon completion of the Pay-Out Note. In signing the Exit Interview Form, the borrower would certify that he was aware of his repayment responsibilities to the loan program and of his indebtedness to the State of Texas.Since payments were to be made directly to the Coordinating Board in Austin, the college (except for minimal collection effort) was to have nothing to do with the collection of loans (13:15).

The Coordinating Board's 1971 policy on enforcement of collection effort stated that:

When any person who has received a loan authorized by the Act shall have failed or refused to make as many as six monthly payments due in accordance with an executed note, then the full amount of the remaining principal and interest shall become due and payable immediately, and the amount due, the person's main last home address, and such other information as may be requested by the commissioner shall be reported by the participating institution to the Commissioner who shall report such person to the Attorney General. Suit for such remaining sum shall be instituted by the Attorney General or any county or district attorney acting for him in the county of the person's residence, the county in which is located the institution at which the person was last enrolled, or in Travis County, unless the Attorney General shall find reasonable justification for delaying suit and shall so advise the Commissioner in writing. (14:18)

On August 31, 1966, the first Texas Opportunity Plan loan was extended to Miss Donna Zenor, a freshman student at West Texas State University at Canyon, Texas. The student was a resident of Canadian, Texas (12:8).

Between 1966 and 1976 many changes in the Texas program have taken place. Some of the major changes were:

- Increases in Interest Rates for Loans. The loan interest was originally set at 6 percent simple interest per annum (12:10). It was to be paid to the state by the federal government while the borrower was in school and up to the time he was placed in repayment status. When the borrower began repaying his loan, he was to pay 3 percent interest and the federal government the remainder. Effective September 1, 1969, the interest was increased to 7 percent; the sharing was also changed. The federal government ceased to share in the payment of the interest once the borrower went into repayment status; it did, however, continue to pay the entire interest while the borrower remained enrolled on at least a one-half time basis up to the time he converted to repayment status (14:14). The interest rate in 1976 was still 7 percent.

- Increase in Bonds Outstanding. Legislation providing for the sale of general obligation bonds of the State of Texas not to exceed $85,000,000, at an interest rate not exceeding 4 percent, was approved by the voters of Texas in 1965. Under this authorization, $10,000,000 in bonds were sold in July, 1966; an additional $39,000,000 of this original authorization was sold by August 31, 1969. However, because of the low interest rate set, the remaining $46,000,000 of authorized bonds could not be sold in the existing market (15).

On August 5, 1969, the voters of Texas approved a constitutional amendment authorizing the sale of an additional $200,000,000 of State of Texas College Loan Bonds. These additional bonds were expected to be sufficient to meet loan demands beyond the capacity of the original authorization then being used. The 1969 bond authorization did set interest rate limitations and issues of these bonds were expected to be sold in combination with some of the originally authorized bonds so that sufficient loan funds would be available for students through the 1975-76 academic year (15).

By August 31, 1970, an additional $1,800,000 of the original $85,000,000 bond issue had been sold; this brought the total bonds sold from the original issue to $40,800,000. Of the 1969 $200 million authorization, $42,200,000 had been sold. This brought the total bonds sold to $83,000,000 (16).

In Fiscal Year 1971, from the 1969 authorization $30,515,000 in bonds were sold. This brought the total bonds sold from this authorization to $72,715,000, and total bonds sold from both authorizations to $113,515,000 (17). Some of the principal of the bonds had been retired during the year leaving a net bond indebtedness of $112.5 million.

To meet the needs of student borrowers, $20 million of State of Texas College Student Loan bonds were sold in 1972 at an average interest rate of 4.89 percent. As of August 31, 1972, the Coordinating Board had sold a total of 135.5 million in loan bonds and had retired $5.5 million of the principal, leaving net bonds payable of $130 million (18).

Subsequent bond sales of $10 million in July of 1973 (19), $15 million in July of 1974 (20), and $13 million in May of 1975 (21) brought the total bonds sold to $175.5 million. However, $15,120,000 of the principal had been retired, leaving net bonds payable balance of $156,380,000 as of August 31, 1975 (21).

- Increases in the Number of Students Served Annually. The increases in the number of students served by the program annually are tabulated following:

During the 1974-75 academic year, 23,197 students borrowed $21,115,242 (32). This number of students and amount of dollars represented: (1) 42,248 (65 percent) fewer student borrowers than in the 1969-70 academic year; (2) only $2,868,530 (10 percent) less dollars loaned than in four years prior to the 1974-75 year.

At the end of the first four years of the Program's operation, the average amount being borrowed by students during their college careers was averaging $1,045 per student (16:102). During the 1974-75 academic year, this amount had increased to $1,414 per student, constituting a 29 percent increase. The average annual loan per student also increased from $367 during the 1969-70 academic year (16:102), to $462 in the 1974-75 academic year (32), an increase of 20 percent. Thus, $8.5 million was required in 1974-75 just to fund the increase in the average size of loan to students. Increases in loan sizes appear to have paralleled rather closely the increases in required costs for attending college between 1969 and 1975 (16:102, 32:173).

- Changes in the Term of the Loan, Grace Period, and Monthly Payments. The period of time a borrower was given to pay out his loan was originally set at five years (13:14). Effective July 15, 1971, this period was increased to ten years, with a maximum limit of 150 years from the date of loan execution (17). The latter extension in time span was designed to allow students on pay-out status but in the Armed Forces or in hardship to postpone their monthly payments for a maximum of three years. Also, the grace period borrowers were given from the time they ceased being enrolled, and the time they entered into repayment status was extended from four to nine months (17). This allowed student borrowers graduating or leaving the institution more time to secure employment and arrange their finances before starting to pay back their loans, and also gave the Coordinating Board more time to prepare the documents necessary to place the student in pay-out status.

Minimum monthly payments were originally set at $15 per month (13:15). For the Fall Semester of 1971, the Coordinating Board increased the minimum monthly payment to $30 per month (13:9).

- Increase in the Maximum Dollar Amount Students Might Borrow. The original limit placed upon the amount one student could borrow was $100, with $1,500 set as the maximum loan in any one year for graduate and 53 professional students and $1,000 for undergraduates (13).On July 15, the maximum total for one student was raised to $7,500, and $1,500 set as the maximum amount a graduate, professional, or undergraduate student could borrow during any one academic year (14:10).

- Change in Program Name. Through a joint resolution, the 6lst Legislature (1969) changed the name of the Texas Opportunity Plan Loan Program to the Hinson-Hazlewood College Student Loan Program. The name was changed, the resolution stated, in order to honor the men who sponsored the original bill in the House and the Senate.

- Change in Lending Procedures. The most drastic change, in terms of procedure, came in January of 13970 when the Coordinating Board adopted two amendments to its Rules and Regulations governing the Hinson-Hazlewood Program. Effective August, 1970, an institution having 10 percent of its borrowers six or more payments behind in payments due would be suspended from making loans; an institution would be placed on probation if its delinquency rate reached 5 percent. Also, all notes by students would require a cosigner except in the case of extreme hardship (16). These two regulations came at a time when the delinquency rate of the program stood at 35.95 percent as of December 31, 1969, and were intended to bring this delinquency rate down (15).

Under the new regulations, cosigners were not only required on all notes but also,

Individual institutions of higher education participating in the program will have more responsibility for administering the program, including

loan collection as well as making the loan. . . .(16)

This charge to institutions apparently had the effect desired. It was followed by a significant increase in loan repayments and a decrease in delinquency rates. By the end of the first fiscal year after the effective date of the new rules, the number of institutions under suspension from participation in the program had dropped from 50 to 14. The rate of accounts six or more months in arrears had dropped to 6.28 percent as compared to 10.08 percent as of November 30, 1969 (16). With the advent of Federal Insurance in September of 19/71, the requirement for cosigners was dropped (23).

- Fluctuation of Delinquency Rates. The proportion of all borrowers with repayments past due for one to five months is usually considered as predictive of borrowers’ subsequent payment patterns. Following are the percentages of delinquency in the one-to-five-months' category at the end of each fiscal year, 1970 through 1975:

Change

Fiscal Years Ending Percent Between Years

August 31, 1970........19.35 (16:102)

August 31, 1971........21.06 (+1.71) (33:86) |

August 31, 1972........16.75 (-4.31) (33:185)

August 31, 1973........11.91 (-4.84) (34:190)

August 31, 1974........10.99 (-0.92) (35:168)

August 31, 1975........15.48 (+4.47) (32:174)

Average of six years...15.92

Of concern to many was the fact that the delinquency rate for 1975 increased by 4.47 percentage points over 1974.

- Conversion to Federally Insured Loans. Another significant development that took effect in the program was conversion to the Federally Guaranteed Student Loan Program. The Coordinating Board had recommended that "appropriate legislative action be taken to permit the program to qualify as an ‘eligible lender’ under the Federal Loan Insurance Program (Title VI-B of the Higher Education Act of 1965, as amended)" under which the federal government would guarantee to the State of Texas the repayment of unpaid loans (16). Staff members began discussing necessary procedures with U.S. Office of Education officials, and steps were launched to obtain the statutory changes necessary to qualify for participation in the Federal Guaranteed Loan Program. These statutory changes were made by the 62nd Texas Legislature session.

Arrangements were then completed for the Hinson-Hazlewood College Student Loan Program to participate as a guaranteed lender in the Federally Insured Student Loan Program. Approval was secured in July, 1971 and federal loan insurance was obtained on all loans made by the Hinson-Hazlewood College Student Loan Program for and after September 1, 1971. The primary effect of the new contractual arrangements was that, through the U.S. Commissioner of Education, the federal government would repay the State of Texas the amount of the student loans outstanding which were delinquent longer than four months. The federal government would then assume responsibility for the collection of those delinquent accounts (17). Also guaranteed were the notes of borrowers who died or became permanently and totally disabled (18).

For a default claim to be paid, federal government regulations require that lenders must prove that due diligence has been exercised in attempts to collect from delinquent borrowers. "Due diligence" is considered to include a telephone contact with the borrower within ten days of the date a payment is missed, followed by frequent written contacts throughout the 120-day period that must have lapsed before the claim is filed. This requirement caused considerable reorganization and supplementation in the previous collection activities of the Coordinating Board's staff (18).

Loans made prior to 1971 (which were not insured by the federal government) were being collected in 1975 through procedures the same as those used for insured loans, except that the Attorney General of Texas was requested by the Coordinating Board to file suit against borrowers when they became six payments past due. To expedite the filing of suits through the Attorney General's Office, the Coordinating Board staff was doing all of the clerical work necessary for suit filing. Court costs and citation fees were paid from Hinson-Hazlewood Program funds (21).

On April 30, 1976, despite rigorous collection procedures and efforts on the part of the Coordinating Board staff, 12,370 (15.25 percent) of the accounts in repayment status were one to five payments past due;10,307 (9.88 percent) of the accounts in repayment status had been referred to the Attorney General for collection; and, 4,604 (3.92 percent) other accounts had been sent to the Attorney General for collection assistance. Combined, 27,331 (29.05 percent) of the accounts were delinquent.

Mr. Mack Adams, Head of the Student Services Division of the Coordinating Board stated to the investigator, “obviously something has to be done to curb the current delinquency rate. What steps will be taken to carry this about remains to be seen” (24).

Section Three: Review of the Literature

A review of the current literature about the Hinson-Hazlewood College Student Loan Program reveals that only one doctoral study has been reported, by Baker Pattillo in 1971. Purpose of that study was to determine if the items of information being requested on the Hinson-Hazlewood Loan Application could be used to identify prospective delinquent borrowers. Findings were that of the 45 application variables compared with delinquency/non-delinquency status, only seven were significantly related at the .05 level of confidence. These seven variables were: the student's summer estimated income; loans of any kind incurred previously; total annual family income; previous receipt of a TOP loan; number of dependents; year of birth; and, possession of life insurance (36:99). Pattillo commented that because of the high delinquency rate and inadequate staff in the Coordinating Board, the Hinson-Hazlewood College Student Loan Program, "is likely to be short lived" (36:44).

Other literature relevant to the present investigation reports the opinions and pronouncements of authorities in student personnel matters and/or results of studies conducted. Extractions from that literature are now presented under eight rubrics.

Financial Counseling

The focal point for most financial aid programs is the student. Consequently, student contact is a major element in the routine of most financial aid offices. This contact may vary in quality and length, but it is always present and necessary. Wrenn states that

the type of aid given to a student varies with, the student's background of experience and present level of development. The application of this principle calls for a careful appraisal of a financial need that is one of a congeries of basic needs–social, emotional, health, vocational and financial. It becomes a counseling problem rather than merely a matter of apportioning available money. (25:381)

Risty points out the crucial role of financial counseling for the student:

. . . the concept for financial counseling is generally a recognition of individual differences in assisting a student in orienting himself to the problem of financing his education, particularly in the direction of independence and high order of personal responsibility . . . .(26:223)

Gross indicates that financial counseling can be considered as counseling only when a cooperative approach to decision making is used and the counselor is sensitive to the meaning of the problem being presented, is capable of transmitting financial aid information, and has taken into account the financial resources available to the student (27).

Considerable assumption appears in literature that the counseling function has qualitative influence upon the repayment behavior of student borrowers. For example, if financial aid counseling is to be effective, it is said the financial aid offices should insure that: "Staff members who have the responsibility for student contact are sensitive to and skilled in interpersonal relations; are knowledgeable of the financial aid programs within the office and the institution; and maintain strict confidentiality of all student information" (28).

Sex, Grade Point Average and Socioeconomic Status of Borrowers

A study concerned with student loan delinquencies was conducted by Dan B. Wolf in a large Midwestern University. The study was designed to determine the extent to which a predictive profile could be constructed from characteristics of students having delinquent loan accounts. Wolf hoped that such a profile would help in reducing future loan risks (29).

The study addressed itself to “those loans due on or before December 21, 1960, but still unpaid as of June 30, 1961." Included in the population studied were c61l loans awarded to 202 students. The original value of the loans was $32,779 and of that amount only $5,645 (17 percent) had been repaid by due dates. Men and women had each repaid only 17 percent of their loans as of the date their loans were due; hence, no differences between sexes in the repayment of loans appeared to exist.

Another part of Wolf's study compared delinquency with grade point average. Using the University's grading system (three points for an "A," two points for a "B," one point for a "C," no points for a "D," and a minus one point for an "F") the study revealed that 7 percent of the delinquent loans had been extended to students with a grade point average between -l and O (F to D) at the time the loan was awarded. Twenty-six percent were extended to students with a grade point average between O and 1 (D to C) at loan granting time. Fifty percent were extended to students with a grade point average between l and 2 (C and B) at loan granting time. Only 1’? percent of the delinquent loans were to students maintaining a grade point average between 2 and 3 (B to A) at loan granting time. (29:123)

In total, 67 percent of the delinquent borrowers (50 percent in the C-to-B, and 17 percent in the B-to-A categories) were maintaining "good standing" grade point averages at the time the loans were extended. Hence, it was concluded that low GPAs were not explanatory of repayment delinquency.

Wolf was unable to obtain enough data from the students' personal records related to socioeconomic factors to include such factors in his study. However, Wrenn had concluded ten years earlier from an investigation that "the relationship between college ability and economic level is not as consistent as is commonly believed" (25:352). His facts indicated that an economically disadvantaged student is no more often a bad loan risk than one not so classified.

Delinquency and Part-time Work

Charles Harrington conducted a study of an emergency student loan program at Ohio University in 1963-64. Its purpose was to isolate characteristics which distinguish students who tend to become delinquent. A sample of nondelinquent borrowers was matched with a sample of those with delinquent accounts. The student record files of the two sample populations were analyzed to locate background factors that were characteristic of each group and which might, therefore, afford a basis for predicting future repayment practices (30).

Harrington found:

- No relationship between variables of sex, or grade point averages, and repayment behavior.

- Positive relationships between non delinquent payees and (1) active participation in high school extracurricular activities carried over into college, and (2) working while attending college.

- Positive relationship between non-delinquency and working at least part-time while attending college.

- Positive relationship between delinquency and failure to receive financial counseling at time of taking out a loan. (30:234)

A study by Bergen and others (37) in 1970-71 concerning Grade Point Average (GPA) and delinquency in the repayment of National Defense Student Loan (NDSL) secured results that conflict with the findings derived by Harrington. The Bergen study was conducted at Kansas state University and used as a sample 1,574 NDSL recipients who had terminated their education at that school prior to September, 1966, and who had established repayment patterns over at least 18 months. GPA classifications were defined as high (3.0 to 4.0), medium (2.2 to 2,9), and minimal (below 2.2). The size of the loan was classified as modest (under $1,500), medium ($1,500 to $2,999), or large ($3,000 or larger). Extent of delinquency was measured by the number of months payments were shown as delinquent on the borrowers’ records.

Findings indicated that borrowers with modest loans had less delinquency than borrowers with medium loans; and that borrowers with medium loans had less delinquency than borrowers with large loans. This was at the level of delinquency of one or more months past due. The size of loan seemed to be positively associated with percentage of delinquency–the higher the loan, the higher the percentage of delinquency.

Borrowers with minimal GPA had a higher repayment record than borrowers with high or medium GPA, in that order, but no significant difference existed between high and medium GPA in association with percentage of delinquency.

Another set of comparisons was run, using a proportion of prepaid loans (i.e., borrower was ahead of schedule) as the dependent variable, with size-of-loan; null hypothesis was rejected. The smaller the Loan, the higher was the proportion of prepayments. With respect to GPA, the highest proportion of prepayments occurred for those with minimal GPA; no difference existed between medium and high GPA subsamples.

Bergen concluded:

Loan officers and committees, if they are concerned primarily with loan repayment, might be justified in using grades as a factor in granting loans... However, the amount which the student borrows during his college career is not a significant factor in predicting repayment habit. (37:67)

It must be noted that this conclusion appears to conflict with Bergen's findings.

Graduation, Academic Achievement and Delinquency

In 1967, George and Patricia Nash conducted a study to discover conditions and factors influencing repayment delinquency of borrowers under the National Defense Student Loan Program. The sample was nationwide, drawn from 1,6/1 colleges and universities (31).

Results indicated that loan recipients who had been forced to leave the institution on academic dismissal tended to have a very high relative incidence of loan delinquency. The authors tentatively concluded that:

Because student loan recipients leaving the institution before graduation and on academic dismissal have a high incidence of loan delinquency, it follows that loan recipients coming to college with a low high school Grade Point Average, or already in college and achieving poorly, could conceivably be higher loan risks. There exists a much greater probability for these students to become academically dismissed. (3l:n.p.)

Type of Institution Attended, Ethnicity, Family Income Level and Delinquency